“UK FinTech is in a great place,” said John Glen; the Economic Secretary to the Treasury as he announced measures last month to make the UK a global hub for crypto.

But the question is whether the actions promised by the UK Government will match the warm words he delivered to an audience of FinTech experts during the Innovate Finance Global Summit in London earlier this year.

If not, the UK’s leading position in crypto could be lost to more favourable jurisdictions.

Sentiment and perception

The UK is home to around 2,000 fintech companies; and London, a melting pot of entrepreneurial minds, financial expertise, investment capital, technology skills and regulators, is second only to the USA as the highest-ranked fintech ecosystem globally.

As part of that, the crypto sector is growing rapidly. One forecast suggests it will grow by more than 7% a year to be worth $2.2 billion by 2026. So, with a highly-skilled, tech-savvy workforce, attractive business and regulatory environments and a flexible labour market, the UK should be in a strong position to capitalise, with sophisticated jobs such as blockchain engineers and cryptocurrency developers.

But, so often in emerging sectors, sentiment can make an enormous difference in how people perceive things. Crypto entrepreneurs and investors – and the decisions they make – will be influenced significantly by the policymakers of the countries in which they do business.

Last month, the Governor of the Bank of England said that cryptocurrencies were the new “front line” in criminal scams, saying the technology created an “opportunity for the downright criminal.”

Contrast that with countries which are bending over backwards to welcome crypto entrepreneurs. Switzerland has perhaps gone the furthest passing blockchain laws and licensing two crypto banks, while Dubai is racing to become a haven for the global crypto industry by offering virtual asset licenses.

The US is making surges too, with President Biden recently ordering the most wide-reaching effort by the federal government to study and potentially regulate cryptocurrencies – an initiative that could see regulators closer to permitting spot cryptocurrency ETFs on the US markets.

In this context then, it’s not surprising that some commentators have suggested the Government’s moves to keep the UK as a leading global crypto hub lag behind many other nations.

The UK’s position

To attract companies, entrepreneurs and investors keen on crypto, the UK needs to commit to investment in a regulatory framework that fosters the national crypto economy and safeguards it without hindering innovation.

The most eye-catching of the Government’s announcements last month, at least as far as the headline writers were concerned, was commissioning the Royal Mint to produce an NFT which will be available by the summer. The Government heralded it “an emblem of their forward-looking approach.”

But beyond that, there were actually some positive moves. This month, the first of several meetings between industry leaders and the FCA, called “crypto sprints” will allow the industry to work with regulators to drive the shape of future regulation. They will also work on a project looking at the legal status of decentralized autonomous organisations (DAOs).

There are moves to look at existing laws governing electronic money which will be adapted to include stablecoins, bringing them within the remit of the FCA and thus paving the way for them to be used as a form of payment.

Finally, blockchain technology, a sector growing so rapidly that the UK simply cannot afford to ignore it. The UK government has announced it will explore the use of Distributed Ledger Technologies (DLTs) in financial markets, create a financial markets infrastructure sandbox and consider using DLTs for sovereign debt instruments.

Welcome steps

From the emergence of Silicon Roundabout in the early noughties to the UK being a global tech powerhouse today – recently valued at more than $1 trillion – entrepreneurs, investors and industry have demonstrated their appetite to use the UK’s attractiveness to international talent and finance to transform it into a hub where nascent technologies and ideas can be transformed into world-class tech businesses.

Crypto is the next step in the UK’s continued growth in digital and technology, it is essential that a world-class infrastructure is built with regulation proportionate to the risk, to boost the modern 21st-century economy and allow crypto to thrive.

The overdraft landscape in the US is at a watershed moment, with banks and credit unions alike taking action to lessen customer impact from overdraft and NSF penalty fees. For a long time, overdraft fees have been ‘in the shadows,’ often perceived as a penalty fee disproportionately applied to those who can least afford to pay.

by Jody Bhagat, President of Americas, Personetics

Market forces and regulatory pressure are moving the industry in a positive direction, and it’s encouraging to see the industry’s rapid response to lessen penalty fee impact with a range of customer-friendly approaches to overdraft response. The range of response thus far can be characterized by the 4P’s:

Policy: Eliminate overdraft fees (Capital One, Ally, Alliant) Price: Reducing or eliminating overdraft or NSF fees (B of A, WFC) Process: Changes to accommodate grace period or negative buffer (PNC Low Cash Mode) Product: Creative enhancements to address the majority of situations (Truist One, Huntington Stand By Cash)

The next breakthrough in overdrafts for the industry is to address the 5t P: Proactive. Proactive cash flow management helps anticipate and resolve overdraft situations prior to occurrence and allows for tailored customer treatments. Rather than determining which fees to reverse, banks can focus on what tailored treatment can help this customer address a future overdraft condition and improve their financial wellbeing in the process. What if overdraft response was something that your institution was excited to promote to customers, in a way that puts the customer at the centre of the conversation?

Rather than simply a defensive move, forward-looking institutions can use this moment as an opportunity to reinforce a customer advocacy approach, where the institution becomes a trusted advisor. With inflation at a 40-year high and many families struggling with cost-of-living pressures, it’s more important than ever for banks to support customers and improve their financial wellbeing.

Here are a few reasons why overdraft response can become a bigger source of differentiation and competitive advantage for financial institutions.

Data is king: A new opportunity to understand your customer

Before you can solve overdraft conditions, it’s important to understand which customers are vulnerable to overdrafts, and what is the root cause. Overdraft conditions can become a moment of opportunity to take a closer look at what is happening in that customer’s life, and engage with the customer in a meaningful, personalized way.

Financial institutions are taking a closer look at which customers are most likely to overdraft, and why. By leveraging advanced data and analytics, banks can proactively engage the 4-6% of customers who overdraft on a monthly basis.

From our analysis, we found four common personas experiencing overdraft situations:

Paycheck to Paycheck: Jim is experiencing multiple cash flow crunch situations every quarter and overdrafts repeatedly. Jim’s income may be volatile or barely enough to cover expenses.

Hardship: Martha has experienced a recent hardship (e.g. income loss or significant medical expense) that is likely to create a near-term overdraft situation and a running up of credit lines.

Mismanaged Timing: Tom has mismanaged the timing of their deposits and payments for a given month, resulting in an overdraft condition.

Affluent Mistake: Jen has plenty of deposits with the bank but unwittingly got caught in an overdraft condition with an account.

Identifying your customer profiles and the context of each overdraft situation can help banks provide the right solution and support for each customer’s financial circumstances. By cleansing and analyzing transaction data, banks can readily understand the context of the overdraft situation. With advanced data and analytics, the bank can identify customers who are at risk for overdraft conditions, and proactively provide treatment options to support the customer’s financial needs, such as an overdraft protection solution with a connected savings account, or a short-term line of credit.

Context is queen: providing tailored treatments for overdraft at scale

Instead of just a penalty fee, overdrafts can be a way to better understand the individual customer and improve their financial well-being. By proactively engaging customers on cash flow issues, banks can reduce the number of overdrafts and negative balance situations and build stronger relationships, leading to higher customer satisfaction and loyalty.

By modelling customers’ cash flow patterns and applying a “robust” balance forecasting algorithm, banks can analyze customers’ historical, scheduled, and patterned activity to accurately identify when they are likely to have a low or negative balance prior to their next likely deposit. That way, banks can help anticipate a customer’s liquidity issues, determine why it is occurring, and proactively provide options to address the situation. Through back testing of our model, we’ve found that we can accurately anticipate approximately 70% of overdraft conditions. With this kind of knowledge, banks can unleash their creativity in offering treatment conditions based on the customer context and the likelihood of overdraft.

Building deeper customer relationships

Overdraft fees have represented a meaningful amount of net income for banks (6-7%) and some have been reluctant to forego that revenue. However, a customer-centric overdraft program could be an even more sizable opportunity for financial institutions by deepening customer relationships

Over the coming year, we’ll see more banks leaning into their overdraft response and seeking a more proactive solution along with reactive actions. Forward-leaning institutions will look at it not as a defensive move to avoid regulatory scrutiny, but as part of a broader proactive approach where the bank operates as a trusted advisor that helps people with their money management.

The time for banks to act is now. As inflation and the cost-of-living crisis rage on, the institutions that adapt their policies with customers front of mind will not only help to improve financial health, they’ll gain lifelong customers in return.

The World Bank cites financial inclusion as one of the key enablers to reducing extreme poverty and boosting shared prosperity. Unfortunately, many countries still fall way behind on levels of financial inclusion and are unable to offer their citizens equitable access to essential financial services. When this occurs, we get financial exclusion. Sadly, this remains an issue around the world, which is preventing nearly 1.2 billion people from fulfilling their true economic potential.

The knock-on effects of financial exclusion are felt by everyone. Essentially, individuals who are excluded from economies are in turn, unable to make meaningful contributions to them. As a result, economic growth in these areas can be limited, which has created a tremendous incentive to promote levels of financial inclusion across the world. In particular, there’s a real need to boost financial inclusivity in regions, such as Africa and Latin America, where the issue may be leading to diminished growth.

Why is financial exclusion problematic?

There are several ways to assess the economic harm caused by financial exclusion. As mentioned, the phenomena contribute to both microeconomic and macroeconomic problems. On a personal level, financial exclusion inhibits a person’s ability to access mainstream financial services, such as savings and pension schemes. Unfortunately, such limitations increase the likelihood of personal debt and limit opportunities for education, personal development and access to employment.

What’s more, financial exclusion overlaps significantly with issues like poverty, as well as broader challenges, such as social exclusion. To this end, without equitable access to financial services, individuals may begin to feel cut off from society. Simply put, these people don’t have access to the same security frameworks afforded to others. Sadly, this can then manifest into a myriad of further economic and societal problems.

Does financial exclusion hurt businesses?

While some of us may be deeply concerned about the plight of the financially excluded, others may feel less concerned as they deal with problems of their own. However, financial exclusion has a negative economic impact on all of us. On the broader scale, financial exclusion can stymy economic growth, lower educational attainment and limit the development of innovation and intellectual property. Directly or indirectly, we all pay an enormous price.

What’s more, the concept of financial exclusion also extends to businesses. In this instance, it applies to companies who are unable to access traditional financial services in the same manner as market competitors. Primarily, this issue tends to affect small-to-medium-sized businesses (SMBs), many of whom find themselves at a disadvantage to larger counterparts when looking to access essential financial services, such as lending capital. Without equitable access to lending capital, the ability of SMBs to reach new markets is severely limited.

Why do SMBs matter?

With high levels of financial exclusion, businesses, as well as the economies they function within, are unable to reach their maximum economic potential. As such, there is a need for all of us to combat the issue. At Uplinq, we believe the fight to promote financial inclusion begins by tackling the issue within the SMB market. If we do that, we can take the first step towards building a more inclusive world for all.

Ultimately, SMBs are the lifeblood of most Western economies, providing around 63% of new private-sector jobs created in the US alone. To properly scale, many of these businesses need access to lending capital, which isn’t always available. Furthermore, on account of their size, many SMBs lack the requisite financial data to pass traditional credit checks. This is not to say these businesses aren’t worthy of receiving lending capital, but instead, simply struggle to effectively make the case within the context of existing decision-making frameworks.

Building a more inclusive world

So, how do we go about building a more financially inclusive world? At Uplinq, we believe a radical overhaul of traditional decision-making systems is required. Specifically, it’s time to update the antiquated decision-making processes used for SMB lending decisions. For too long, these services have relied on limited data sets to generate results. As such, many existing systems are unable to offer an accurate picture of a businesses’ true financial viability, which limits lending opportunities.

Thankfully, modern technologies now exist, which offer dramatic improvements in this area. Notably, solutions like Uplinq can assess billions of alternative data points to create a more comprehensive picture of a business’ financial viability, regardless of its size or status. By implementing these technologies within their systems, lending companies can begin to serve the SMB market in a far more inclusive manner.

If we can achieve this goal, then we can begin to build a more inclusive world, which will benefit us all. This is the objective we’re working towards every day. Our innovative solution can allow credit lending providers to generate the most accurate lending decisions possible. To this end, our solution can help a greater number of SMBs receive lending when they need it most, helping to close the gap between them and their more established counterparts.

Mastercard recently announced it is trialling a new biometric card that will allow businesses to offer consumers the opportunity to pay via biometric services through an app. It’s a conversation that’s been on the radar for some time now, particularly as a means to eradicate the need for passwords. And it’s not a bad idea in theory. HSBC found that fraud was reduced by 50% when using a voice authentication system for customers. What’s more, Mastercard’s trial promises the ability to speed up payments, reduce queues, and offer more security than a standard credit or debit card.

With such benefits on offer, it’s not surprising that the biometrics market is expected to be worth $18.6bn by 2026.

Though the question must be asked as to whether we are hyping yet another technology up a little too much too soon. Biometric payments, still very much in their infancy, in my opinion, have a long way to go before becoming mainstream, with several obstacles to overcome first.

Prepare to fail

Facial recognition, while of course a huge innovation and one that has changed the game for many use cases, is not without its problems. As most of us have now come to realise, it’s not perfect and our recognition systems continue to fail to work 100% of the time. While error rates are now less than 0.1% – a seemingly low percentage – it’s one that translates into potentially thousands of transactions when considered on a global scale.

To reduce the chance of failure, companies will need to have access to several different forms of authentication, such as fingerprints, vein patterns, iris scanning, facial recognition and more to offer multiple options when consumers experience problems. While reducing the risk of errors and fraud, each system has its own accuracy rates and problems that firms need to be aware of. For example, facial recognition can sometimes be thrown off by glare from glasses, and vein pattern relies on high-quality photos in the first instance and ensures that subsequent scans are not affected by different light conditions.

Unfortunately, though, the issues with biometric data and systems don’t end with our phones occasionally not recognising who we are mid-yawn. For example, its use by police establishments has been a huge cause of concern for citizens, rightly worried about unknown entities having access to so much of their personal data.

The ultimate trade-off

And that is perhaps the biggest obstacle to overcome in order to make biometric payment systems mainstream. The trade-off for consumers to ensure they are a success is that companies will have to have access to an increasing pot of every individual’s personal data. There’s no compromise here; personal data is simply fundamental to how the technology operates.

Such a big concern for the increasingly data-aware citizen means high stakes for any business wanting to get in on the biometric payments action. For instance, while a data breach today may result in passwords and usernames being leaked, this information can be changed and updated relatively quickly and easily. Biometric data, unsurprisingly, is impossible to change.

And it’s not just bad actors in the cyber world that consumers are or should be worried about. Sharing such sensitive and personal information with global corporates, should never just be a given especially for those which aren’t clear on how that data will be used. For example, in countries with less protection for individual rights, such as China, the facial database could be used to identify and target certain groups of people by the state authorities, as has already been seen with the Uighur people. If the public becomes distrustful and refuses to share information with payment firms as a result of such events, any biometric technology beyond just unlocking a smartphone will struggle to get off the ground in a meaningful way.

It’s down to businesses and governments to overcome these concerns by putting the appropriate regulations and processes in place that protect consumer data and put their minds at ease. This will help build trust in new technology. What’re more governments around the world need to be communicating effectively to create conformity across countries on how data should be handled and secured. Firms in turn will benefit from being able to focus on one set of rules, in the knowledge that the rights of people in different locations are being protected.

Who foots the bill for biometric payments technology?

Beyond consumer concerns, there’s an issue of cost. New technology doesn’t come cheap – so who’s responsible for paying for the new devices that will be required to make biometric payments a reality? We’re talking billions; at the moment some high-end biometric systems can cost up to $10,000, a significant and completely unrealistic cost for small business owners.

And for what? While biometric payments may well make things a little easier and quicker for consumers, it won’t win or lose their loyalty when they can just pay by other means, so there’s simply no ROI. Only when it becomes an expectation of consumers, instead of simply a novelty, will it become important for companies to jump on the bandwagon. But that could take years, at least until the technology becomes an affordable price where it is feasible for companies to make this investment. Until then, widespread adoption is a distant notion.

We need to take a step back

There’s no doubt that schemes like Mastercard’s will crop up more frequently – innovations like these are part and parcel of today’s digital world and it’s exciting to see what the future could look like. But the point here is that, once again, we’re getting a little ahead of ourselves. Privacy issues, in particular, prove a huge obstacle, not just to payments, but to all other systems attempting to make use of biometric data. The regulations required to fix the issue could take years to get right.

So, just like we won’t see flying cars zooming overhead tomorrow, biometric payment systems have a long way to go before becoming mainstream.

As nations worldwide continue to sanction Russia in condemnation of their invasion of Ukraine, companies have now joined the movement to exclude the Russian government – and sometimes Russians – from their list of clients. Some of these companies have decided to ban them following international sanction provisions from The Office of Foreign Assets Control (OFAC).

Others have taken this decision as a show of solidarity with the Ukrainian people. However, not all FinTech companies are placing blanket boycotts on Russian citizens. The most notable holdouts are Binance and Kraken, citing the argument that banning “innocent Russians” goes against the philosophy behind cryptocurrencies.

So, let’s go through the reactions of fintech companies to the Russian invasion and explore how they affect the socio-economic climate in Russia and the rest of the world.

SWIFT

As pressure mounted on SWIFT to respond to the Russian invasion, the payment network obliged by suspending 7 major Russian banks from performing transactions indefinitely. The ban stops these Russian banks from accessing their global economic resources, but the country has outlined measures to combat the hard-hitting impacts of the SWIFT suspension. In anticipation of incoming economic sanctions, the Russian government developed SPFS (System for Transfer of Financial Messages) — a SWIFT equivalent that works only in Russia and some banks in Switzerland, Kazakhstan, Azerbaijan, Cuba, and Belarus.

Russia now has to rely on China’s more formidable Cross-border Interbank Payment System (CIPS) for international transactions.

VISA

According to Statista, VISA owns 12% of all credit payment cards in the world (335 million credit cards), accounting for about 50% of the overall market shares. The company reacted to the Russian invasion by halting all its operations within Russia and banning Russian VISA cardholders from processing transactions.

According to VISA’s official statement, the company is ‘taking prompt action to ensure compliance with applicable sanctions, and is prepared to comply with additional sanctions that may be implemented’. The VISA Foundation has also donated a $2 million grant to the US Fund for UNICEF to provide the Ukrainian people with humanitarian aid.

Mastercard

Mastercard has maintained the same ironclad stance as VISA on the Russian invasion. The credit card company has reportedly forfeited about 4% of potential revenue by excluding Russians from its services.

Mastercard CEO Michael Miebach released a statement saying that the company has ceased operations in Russia, as well as banned certain Russian banks from the payment network. Miebach also affirms that the company has sent a $2 million humanitarian fund to the Red Cross, Save the Children, and employee assistance.

Amex

American Express has also joined the ranks of Visa and Mastercard in suspending all operations in Russia and Belarus. According to a memo from American Express CEO Stephen J. Squeri, the cards issued in Russian territory will no longer work in Russia or outside the country. As part of Amex’s “Do What is Right” code, the company has pledged $1 million to humanitarian organizations to provide relief to people in Ukraine affected by the war.

Source: Mykhailo Fedorov (Ukraine’s Deputy Prime Minister and Minister of Digital Transformation) on Twitter

PayPal

PayPal has also halted all operations in Russia until further notice. Dan Schulman, PayPal CEO, released a statement saying: “PayPal supports the Ukrainian people and stands with the international community in condemning Russia’s violent military aggression in Ukraine. The tragedy taking place in Ukraine is devastating for all of us, wherever we are in the world.” He goes on to add that despite banning Russians from using PayPal’s services, the company will still provide support for Russian citizens within its workforce.

Payoneer

Payoneer’s reaction was to stop all issuance of cards to customers with postal or residential addresses within the Russian Federation. According to the company’s updated FAQs, Russian citizens with Payoneer cards issued outside Russia can still conduct transactions without restrictions.

Upwork

In an open letter to freelancers, Upwork CEO Hayden Brown reiterated the company’s mission to help improve people’s lives. As a result, with over 4% of registered freelancers from Russia and Belarus, Upwork has suspended operations and has shut down support for new business generation in both countries. To this end, the changes will take full effect on 1 May 2022, leaving freelancers and clients in Russia and Belarus unable to create new accounts, initiate new contracts, and appear in searches. The platform also donated $1 million to Direct Relief International to support Ukrainian citizens caught up in the war.

Revolut

As a company with a Ukrainian co-founder Vlad Yatsenko, Revolut has provided unwavering support for Ukrainians suffering from the war. The current CEO Nikolay Storonsky, born in Russia to a Ukrainian father, released an open letter, categorically condemning the war, saying that ‘this war is wrong and totally abhorrent’ and that ‘…not one more person should die in this needless conflict’.

In a statement titled The War on Ukraine: Our Response, Revolut has affirmed its dedication to uphold and impose sanctions placed on Russia. As part of its support to Ukraine, Revolut has removed transfer fees for every transaction going into the country. The company has also pledged to match every donation made to the Red Cross Ukraine appeal.

Stripe

Although Stripe does not work in Ukraine, Russia, or Belarus, the financial services and SaaS company has pledged to impose sanctions on the Russian government and its citizens. The extent of this ban will cover transactions using the Mir payment system, as well as services linked directly or indirectly with the Crimea and the separatist Luhansk and Donetsk regions.

Paysera

Paysera has released a comprehensive list of financial restrictions on Russia and its allies involved in the Ukrainian invasion:

Russian citizens will no longer be able to use Paysera (this restriction does not apply to Russian citizens with residency or work permits in other supported countries).

All current accounts belonging to Russians will be closed.

Russian and Belarusian companies are banned from using their Paysera accounts.

All current business accounts belonging to Russian and Belarusian entities will be closed.

Transactions to Russian and Belarusian banks between private individuals will continue but must go through rigorous verification procedures.

Paysera will roll back all money transfers from Russian and Belarusian banks received on Monday (23 February and later).

Paysera users can no longer exchange to Russian Roubles (RUB).

This list is only one part of the extensive regulation changes for Russian citizens and banks. For more information, read the entire press release.

Apple (Apple Pay) and Google (Google Pay)

Apple and Google set rivalries aside to impose a collective ban on the Russian government and its citizens for their actions in Ukraine. According to NPR, Apple will stop shipping products to Russia with immediate effect. This announcement sent shockwaves around the tech world because of the company’s global influence.

In the same vein, Google has also removed media platforms RT and Sputnik from its services, banning their content within EU countries.

But that’s not even half of it. Apple has furthered its crackdown on Russia by deactivating its payment service Apple Pay in the region – 29% of Russians rely on Apple Pay for contactless payments. Similar to Apple, Google Pay (used by 20% of Russians) has also ceased all digital payments by Russian citizens within occupied territories.

Money transfer services

According to Statista, the value of cross-border money transfers made by Russians in 2020 were worth over $40 billion, which is by almost $8 billion less than in 2018. In 2022, however, this sum is likely to be much lower taken the situation with the money transfer services that are leaving the Russian market.

Western Union

On 10 March 2022, Western Union issued a press release announcing that all the company’s operations in Russia and Belarus will be suspended with immediate effect. For the people of Ukraine, Western Union has created a donation portal to address the humanitarian and refugee crisis, according to Elizabeth Executive Director of the Western Union Foundation.

The money transfer company has pledged $500 000 to provide humanitarian aid to the Ukrainian people. To donate to the Western Union Foundation, visit its official website.

Wise

Before the 2022 Russian-Ukrainian war, Wise (formerly TransferWise) had already placed a $200 limit for Russian account owners. With the current swathe of sanctions, the remittance and payments company has doubled down on its restriction for individuals and businesses within the Russian Federation and its (illegally) occupied territories.

Find a detailed breakdown of the restrictions according to the company’s Help Centre below:

You can only send RUB to private bank accounts or cards in Russia.

You cannot send RUB to government agencies in Russia.

You cannot send RUB to Crimea or Sevastopol.

You cannot send USD or EUR to accounts in Russia.

MoneyGram

According to Quartz, MoneyGram still works both in Ukraine and Russia since the sanctioned banks — Sberbank (Russian) and VTB — are not involved in the transactions directly. This same report also shows that, on the first day of the invasion, US-based remittances to Ukraine spiked 120%, while the number rose to 50% in Russia. Nevertheless, MoneyGram has removed all fees on transfers going to Ukraine from the US, Canada, and EU.

Remitly

Remitly is a P2P service that allows immigrants to send money across borders. Since the company’s core demographics (immigrants) are closely aligned to the plight of Ukrainian refugees, it is no surprise that tit has also banned Russia. Remitly, through a spokesperson, has communicated its dedication to upholding this ban according to the EU and US sanctions.

Source: World Remit on Twitter

Zepz (WorldRemit)

Zepz, formerly WorldRemit, has released a list of countries on its banned list, including Russia and Belarus. The company also released an updated list of transaction conditions, showing that Russia is on the blocklist until further notice.

“The Big Four”

Members of the Big Four — Deloitte, Ernst & Young, KPMG, and PwC — have also enforced the sanctions imposed on Russia by the US and EU nations. At the time of compiling this report, the aforementioned companies are not in a hurry to impose blanket sanctions on all Russian citizens since a combined 1.1% (around 13000 people) of their global workforce is in Russia.

Deloitte’s Global CEO Punit Renjen said: “Last week, Deloitte announced it was reviewing its business in Russia. We will separate our practice in Russia and Belarus from the global network of member firms. Deloitte will no longer operate in Russia and Belarus.”

Mark Walters, KPMG’s Global Head of Communications, said: “KPMG has over 4,500 people in Russia and Belarus, and ending our working relationship with them, many of whom have been a part of KPMG for many decades, is incredibly difficult.”

Mike Davies, PwC’s Director of Global Corporate Affairs and Communications, PwC UK, said: “As a result of the Russian government’s invasion of Ukraine, we have decided that, under the circumstances, PwC should not have a member firm in Russia and consequently PwC Russia will leave the network.”

EYreleased a statement that said: “Today, EY global organisation decided that the Russian practice will continue working with clients as an independent group of audit and consulting companies that are not part of the EY global network. The changes will take effect after the required transition period.”

Source: Mykhailo Fedorov on Twitter

The crypto world

Although the major players in FinTech are equivocal in their condemnation and boycott (full or partial) of Russia, the crypto community maintains partial neutrality. The overarching sentiment within the world of crypto is that private citizens should not suffer due to the actions of their governments. After all, some of these individuals might be using cryptocurrencies to oppose tyrannical regimes.

Notwithstanding, the Russian Central Bank has proposed a ban on mining and trading cryptocurrencies. With Russia occupying third place among Bitcoin mining regions globally, the impacts on the value and volatility of the crypto market might be extensive.

On its part, Ukraine has also used crypto assets to fund its defence against Russian aggression. Ukraine’s Deputy Prime Minister Mykhailo Fedorov has also posted wallet addresses for the Ukrainian Army and Civil Defense support.

Source: Jesse Powell on Twitter

Kraken

CEO of Kraken, Jesse Powell released a Twitter thread in response to the Ukrainian Prime Minister’s call on crypto exchanges to block addresses of all Russian users. In the thread, he expresses regret for the appalling conditions Ukraine finds itself in at the hands of its aggressive neighbours. However, he insists that the company cannot blanket-ban citizens ‘without a legal requirement’ to do so.

Binance

Binance CEO, Changpeng Zhao, released a detailed statement refuting claims that ‘Binance doesn’t apply sanctions’. He expressed that Russian individuals banned by US and EU sanction regulations are not allowed to trade on Binance.

KuCoin

KuCoin CEO Johnny Lyu also refuses to freeze the accounts of Russian users, unless there is a legal precedent to do so on a case-by-case basis.In a statement to CNBC, the CEO expressed KuCoin’s stance on the issue: “As a neutral platform, we will not freeze the accounts of any users from any country without a legal requirement. And at this difficult time, actions that increase the tension to impact the rights of innocent people should not be encouraged.”

Source: Brian Armstrong on Twitter

Coinbase

According to Coinbase’s Chief Legal Officer Paul Grewal, the company has blocked over 25000 accounts linked with “illicit activity” with the Russian government and its allies. While the crypto exchange is dedicated to helping the Ukrainians, they refused to freeze the assets of ‘ordinary Russians’.

Nevertheless, Coinbase has implemented measures to monitor attempts by sanctioned individuals to evade the restrictions. The crypto exchange will also follow recommendations that align with government recommendations, provided they don’t interfere with individual rights.

Adyen

Although the Ayden network does not work in either Russia or Ukraine, the company has decided to offer humanitarian help to the victims of the ongoing invasion. Adyen’s policy decisions include:

Blocking sanctioned banks and private entities

Suspending US and EU processing services in Russia, Crimea, and the separatist regions in Donetsk and Luhansk.

Suspending transaction processing in Russian rubles (RUB) regardless of issuing country.

To the Ukrainian people, Adyen has pledged humanitarian support through Adyen Giving and other charities like the UNCHR Disaster Relief Fund, Giro 555, and the Red Cross.

Mintos

The loan management platform Mintos has removed loans from Russian and Ukrainian lending platforms as a ‘cautionary measure’ to protect lenders from the unprecedented repercussions of the invasion. As part of the Mintos Conservative Strategy, the company will uphold these restrictions until the conflict stabilises – or ends.

eToro

When eToro announced that it would be force-liquidating Magnit PJSC stocks (and other related Russian stocks), they probably didn’t expect such a massive amount of pushback from users who had equities in these companies. As a result of the criticism and public outcry, the company refunded all affected parties, except for leverage stakes. Despite the earlier wave of backlash, eToro is still considering what to do with nine other stocks from the country, including Sberbank of Russia, Rosneft (RNFTF), Gazprom, and Lukoil.

Conclusion

The Russo-Ukrainian war has plunged the entire financial sector into a new reality, which follows post-pandemic inflation. We are now witnessing an unprecedented situation – financial institutions and FinTech companies are reacting in real-time to impose sanctions and boycotts on Russia and its citizens. Numerous companies that aren’t obliged by law or sanctions have taken the initiative to leave the Russian market. These decisions cost each of them a significant part of revenue, yet they demonstrate the willingness to pay this price in order to help stop the war.

FinTech is synonymous with innovation and is a key industry in this country. Its influence spans the globe, however, and makes it a primary player in the move towards greater financial and environmental sustainability.

by Keith Tully, Real Business Rescue, a company insolvency and restructuring expert.

Corporate social responsibility has been a pivotal business model for decades, but the 2021 COP26 Climate Change Conference in Glasgow clarified the urgency to act with purpose and laid out in stark detail the consequences for the planet if we don’t.

The FinTech industry is ideally placed to use its prominent standing on the global stage, therefore, and positively influence the crucial issues we face. It can set a ‘green’ example for others to follow, ensuring businesses adopt sustainable practices and leading the way towards a lower-carbon future for industries across the board.

How can Fintech businesses take a stand on sustainability?

Operate a ‘green’ supply chain

Fintech’s inherent use of big data, artificial intelligence, and real-time information, makes the industry a perfect role model when implementing environmentally friendly and sustainable logistical practices.

Transparency and collaboration between supply chain members is a necessity for a ‘green’ supply chain to work, and this ultimately reduces waste and increases cost-effectiveness for all participants.

Develop ‘green’ technologies

The industry continues to provide cutting-edge solutions that streamline and modernise financial procedures and payment systems, and can positively influence corporate behaviours.

Brand reputation strengthens when businesses use innovative financial technologies – they become trustworthy within their industry and in the eyes of the wider community. The investment in ‘green’ solutions consolidates the drive for sustainability and enables ethical conduct and business behaviours to be put in place.

Innovative banking and payment solutions

The banking and payments industries have transitioned, almost beyond recognition, in the last few decades. Although the ‘traditional’ high street banking services are still available, the development of new financial technologies has created a thoroughly modern alternative for businesses and individuals.

The Fintech industry has developed highly sophisticated, cost-effective, and sustainable banking and payment systems that help businesses reduce their carbon footprint. Blockchain is one such example, and this provides a platform that supports other technologies such as new payment and finance solutions.

Data analytics

Big data provides in-depth perspective and insight into various areas of business and offers key decision-makers a solid foundation for making strategic plans. It can also be used to keep a business on track towards financial and environmental sustainability.

Global financial services group, BBVA, uses technology to help organisations calculate their carbon footprint using data analytics, for example. Businesses can calculate their carbon footprint and then register on The Carbon Footprint Registry.

The ‘Climate Registered’ seal placed on their websites and promotional materials demonstrates the business’ commitment to sustainability, and to reducing their carbon footprint.

Make sustainability the USP

Adopting good practices and promoting financial and environmental sustainability enables Fintech companies to differentiate themselves, and to stand out in an increasingly crowded industry.

Making sustainability their unique selling point within a ‘Green Fintech’ umbrella of innovative technologies and working practices reiterates the drive to help tackle climate change whilst promoting a sense of purpose and well-being among staff.

Sustainable financial products

Figures published by Statista show how significantly Fintech solutions have changed the way in which we bank and carry out our financial business as a nation.

In 2007, only 30 per cent of banking customers regularly used digital banking services, a figure that has risen to 76 per cent in 2020. Personal finance budgeting and investment apps also help people achieve their own individual goals for sustainability.

Fintech businesses can measure and verify the impact of sustainable financial products, such as ‘green’ bonds, loans, and investment funds, and make adjustments as necessary to improve the products.

The case for taking a stand on financial and environmental sustainability

The positive case for taking a stand on sustainability is clear. It’s what is needed if we are to head off total climate catastrophe. This movement also holds significant benefits for individual businesses in terms of their reputation and place in the community, however.

Sustainability is an issue close to people’s hearts, and staff can rally around such a cause. This increases morale and creates an inclusive working environment that promotes well-being and productivity.

Apart from the key benefit of creating a more sustainable operating environment for businesses within the industry, Fintech’s considerable influence could also affect far-reaching change in other industries.

In fact, Fintech is in the perfect position to lead on financial and environmental sustainability. Introducing new ‘green’ financial products and creative payment systems not only helps other businesses on a practical level, but also sets the high environmental and financial sustainability standards that we need, and that others will follow.

Like most criminals, cyber hackers want an easy life. Just as burglars prefer forgotten open windows over picking front door locks as a way in, so their digital counterparts are looking for targets that offer maximum return for minimum effort.

As such, while major corporations wise up to the threat of sophisticated attackers and invest in the sort of defences that limit the impact of bad actors, criminals are now turning their attention to potentially easier targets. And that includes businesses that are raising capital or those that recently announced funding – particularly when those businesses not only hold significant financial data but also potentially offer gateways, or open windows, to other companies.

It’s thus no surprise that ransomware attacks are increasingly targeting Private Equity (PE) firms and their portfolio companies (PortCos). As attacks increase, it’s imperative that investors become more aware of the risks they face and take swift action to protect themselves – and their portfolio companies.

Cyber vigilance as a differentiator

Cyber vigilance is increasingly becoming a differentiator for investors when considering companies to add to their portfolios. Gartner highlighted that “by 2025, 60% of organizations will use cybersecurity risk as a primary determinant in conducting third-party transactions and business engagements,” and in doing so noted that “Investors, especially venture capitalists, are using cybersecurity risk as a key factor in assessing opportunities.”

There’s also regulatory pressure to get houses in order. In February, the Securities and Exchange Commission (SEC) voted to propose a new set of cybersecurity rules to oversee how alternative investments or private capital firms manage risk, requiring clear policies and procedures to be put in place. In addition, advisers would need to report incidents that impact their firms, funds or clients.

Clearly, PEs need to be as rigorous in checking their own windows are closed as they are in running the rule on the security posture of target companies. For most, it means a wholesale change in their approach to cyber security. The question is, how do they begin to implement this new approach? Securing your own operations is hard enough – how do you extend that to other entities in your orbit?

Check your windows

First, it’s worth considering what open windows there could be. One of the most glaring yet overlooked open windows is the employees at PEs and their PortCos. This isn’t to suggest that everyone is maliciously trying to undermine their employer (though insider attacks do happen), more that too often an assumption is made that workers understand the ways in which they can be targeted.

The reality is that many people don’t realize how many cyber threats are designed to exploit people’s ignorance or naivety. From ransomware to phishing attacks, many of the major leaks we read about in the news can be traced back to individuals who didn’t realize they shouldn’t click on a link, open a suspicious attachment or download an app at work.

Like any good burglar- why would a cyber thief spend time trying to crack encrypted corporate networks when they could simply gain access by targeting unsuspecting employees? They wouldn’t. That’s why

the first step in any PE firm’s cyber security approach should be to focus on educating staff, starting with the PE firm itself and then extending out to its PortCos to ensure they are undertaking similar processes.

Similarly, it’s not too difficult for attackers to take advantage of a lax approach to updating software. Technology is constantly evolving, and changes to critical systems can bring immense business benefits and operational efficiencies – but can also create new gaps in defences. PE firms and their PortCos must ensure that they have a rigorous and consistent process to keep systems up to date and fix bugs as solutions are released to prevent attackers from exploiting any holes.

Sophisticated responses for new attacks

Those are just two of the windows that can be closed relatively quickly. But the fact is that attacks are becoming more sophisticated, which means the responses must too.

Only real-time cyber risk monitoring will enable firms to protect their most sensitive data and safeguard against internal and external threats. That means firms must have more than the traditionally adequate technical and logical controls – they need active, continuous risk mitigation solutions and reporting, and cyber programs that are tested using real-world scenarios that provide a clear picture of how the business would defend against and respond to an incident.

A case of when, not if

Ultimately, PE firms and their PortCos need to realize that it is a case of when, not if, they are targeted. Most businesses understand and accept it; what they will not accept is inaction, attempts to hide issues, or a failure to mitigate the impact.

That’s why the new SEC rules are pushing for incidents to be reported, and why the European Union’s General Data Protection Regulation (GDPR) has fines in place for companies that have not done everything they can to reduce the risk of data breaches. Those businesses that do not do everything in their power to respond appropriately to incidents will not only have to deal with the immediate fallout of the attack itself, but subsequent legal, financial and reputational consequences.

Close the windows to protect firms and PortCos

It’s one thing to be undone by a sophisticated attack that may be far ahead of any of your existing defences; it is quite another for an opportune bad actor to sneak in via an open window. Cybersecurity is challenging, and it’s only becoming more complicated as attackers become more sophisticated and geopolitical threats rise. It’s clear that if there was ever a time to pay attention to cyber risk and buttress your defences, it is now.

The best way for PE firms and their PortCos to protect their organizations is to make it as hard as possible for cyber attackers to gain access. Invest in the right real-time cyber risk monitoring, confirm all your systems are patched and up to date and have your comprehensive incident response plan tested and ready to go on a moment’s notice. Put simply: Don’t be an open window.

Globally in 2020, more than 70 billion real-time payment transactions were processed – an increase of 41% compared to the previous year.

by Charles Sutton, Financial Services and FinTech Lead EMEA, Nvidia

This massive rise in transactions has presented an opportunity for criminals to conduct more fraudulent activities like account takeovers, chargeback fraud, or identity theft, resulting in more than $1 trillion stolen in cybercrime activities in 2020 alone.

NVIDIA’s 2022 State of AI in Financial Services survey found that implementing artificial intelligence (AI) is one way financial institutions protect their customers, data, and bottom line.

Top trends for AI in financial services

Given the vast increase in fraudulent activity, it’s unsurprising that the top AI use case identified by financial services professionals is for fraud detection. 31 percent of respondents use it to protect customer payments and transactions, up from just 10 percent in 2021.

Conversational AI, a type of AI where humans can interact naturally with machines by simply conversing with them, entered the top three use cases this year with 28 percent of respondents using it, followed by 27 percent using AI for algorithmic trading.

Compared to 2021’s survey results, 2022 shows a significant increase in the percentage of financial institutions investing in AI. Conversational AI increased by 8 to 28 percent, know your customer (KYC) and anti-money laundering (AML) fraud detection rose from 7 to 23 percent, and recommender systems increased from 10 to 23 percent.

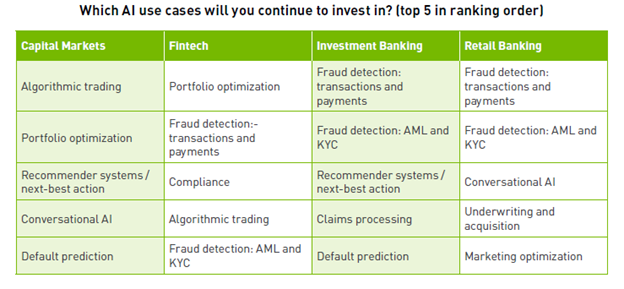

What AI use case is your company investing in?

There are many uses for AI across the financial services landscape.

The report shows that fraud detection of transactions and payments is key for fintech, investment banking, and retail banking institutions. Conversational AI is a priority for capital markets and retail banking, and recommender systems are important for capital markets and investment banking.

Conversational AI for fraud detection and more

Increased fraud attempts have a significant impact on operations, so naturally, it falls high on the priority list for most financial institutions.

Natural Language Processing (NLP) is a form of conversational AI that can be leveraged across KYC and AML. An NLP algorithm can be trained to know everything about a customer – their spending habits, financial histories, unique risk factors, and even voice and behavioral biometrics – to reduce the risk of money laundering and other types of fraudulent activities.

It’s not all about fraud, though. NLP can also be used to optimize and transform the customer experience. Customer experience is incredibly important. In fact, just a one-point decline in a business’ customer experience score can equal $124 million in lost revenue for multi-channel banks, according to Forbes.

In an increasingly 24/7 world, and with a growing volume of customer calls, virtual assistants can be on call day and night to assist with simple inquiries such as account-related questions or product applications. UK-based NatWest’s digital assistant, Cora, is handling 58% more inquiries year on year, completing 40% of those interactions without human intervention. According to Jupiter Research, virtual assistants and chatbots are expected to result in savings of $2.3 billion by 2023.

NLP can also be used for recommender systems. It can generate personalized, recommended offers and next-best actions for each customer based on their individual data.

What does the C-Suite think?

The State of AI in Financial Services survey includes financial professionals across various roles, from c-suite to developers, IT leaders, and managers. This perspective allows for a broader understanding of how groups within an organization perceive their AI capabilities. The survey found that 37 percent of the c-suite view their AI capabilities as industry-leading, whereas only 20 percent of developers have the same perception.

When looking at the challenges organizations face when trying to achieve their AI goals, the c-suite, developers, and IT are unanimous on their concern for lack of data, lack of budget, too few data scientists, poor technology infrastructure, and explainability.

Creating Exponential Value with AI

Knowing a challenge means it’s possible to find a solution. There are several steps companies can take to improve the impact AI can have on customer satisfaction, operational efficiency, and revenue growth.

Successfully moving AI into production is an area of opportunity for organizations, which the survey found that only 23 percent of organizations currently think they can carry out. Knowing the target business outcome, identifying key performance indicators for measuring success, and building the research project as a pilot so that workflows are in place are best practices organizations can implement to improve their ability to scale AI applications into production.

Just 46 percent of organizations use explainability in their AI and machine learning operations. Supporting explainability is critical to integrate into a firm’s overall AI governance practice and doesn’t always need to be done in-house for teams that don’t necessarily have the right expertise.

Pursuing ethical AI is the third opportunity highlighted in the report. Only 26 percent agreed that their organization understands the ethical issues associated with AI and proper governance. Bias, data management, model maintenance, and explainability are crucial aspects of an AI governance framework. Environmental, Social and Corporate Governance (ESG), a way of measuring an organization’s ethical properties, is also growing in popularity within financial services and is a crucial element of ethical AI.

What’s next for AI in financial services?

The future is looking bright for AI. Hiring more AI experts, providing AI training to staff, engaging with third-party partners to accelerate AI adoption, investing more in AI infrastructure, and identifying additional AI use cases are in the works for at least 30 percent of respondents. And the expected outcome is clear, with 37 percent believing that AI will become a source of competitive advantage for their organization.

According to the survey findings, there are many use cases, all of which are growing tremendously year on year. Organizations are aligned on their challenges and committed to investing in their AI strategy to achieve greater customer satisfaction, lower operating costs, higher revenues, and an overall competitive advantage.

Over the course of time, supply chains have evolved and become ever more complex and multifaceted. Where once they were local, or domestic, supply chains are now global. Whilst this drives down per unit costing through comparative advantage, it does mean that businesses need entire departments to source high-quality components for onward processing and distribution. They must also work to maintain positive relationships with suppliers during the procurement and supply chain process.

by Alistair Baxter, Head of Accounts Receivables Finance, Taulia

The changing dynamics of the world around us, whether that be economic or political, mean that we often see a play-off between market protectionism and free trade economics. Events of the last few years combined with various trade measures have significantly disrupted, and ultimately changed forever, global supply chains.

Alistair Baxter, Head of Accounts Receivables Finance, Taulia

We have observed an increase in global disruptions to supply chains in recent years, particularly during the Covid-19 pandemic – and the impact of that disruption cannot be overstated. Increased shipping costs are now the norm and supply chains are being remapped by companies to try and gain an advantage over competing supply chains. This was brought to the mainstream attention when one of the world’s largest container ships, the Ever Given, whose onboard goods totalled $775 million, blocked the Suez Canal for 6 days in 2021. This form of trade friction has created disruption which negatively impacted businesses and economies and while Ever Given was a first, it may seem obvious to say that it might not be the last and businesses need to be prepared.

Resilience is now a key challenge for those responsible for sourcing and securing strong supply chains. Technology has a massive role to play in supporting this and alleviating some of the current complex challenges. Technology can paint a clear picture of where the disruptions are, or even better, predict where they might happen further down the line, beyond the current field of vision. Continued adoption of technology will dynamically allow information to flow down to suppliers – otherwise known as ‘purchase order cascades’ – to increase transparency for even the smallest suppliers.

The world of supply chains has an opportunity to lead the way in ESG by increasing communication and transparency. Technology is again the enabler, allowing for the tracking and rewarding of supplier ESG performance. It is imperative that those at the very top of the supply chain set the ESG tone and support the raising of standards throughout their supply chains. Working together will improve the supply chain ecosystem for the long-term.

Supply chain managers have a significant role to play in the reshaping of industry. In response to the purchasing habits of consumers in developed markets, it’s the best value chain that wins, as opposed to the best product or retailer, as customers come to expect prompt delivery of goods, or ESG credentials to be made clear at point of purchase. Amazon, as an example, has one of the best value chains: logistics, ease of access, and customer touch points are all carefully considered and planned. Amazon has been acquiring its own shipping containers since 2018 and chartering its own ships to avoid major bottlenecks in its supply chains and to get products onto e-shelves.

Technology has been developed to respond to this shift in behaviour and as hyper-personalisation and emotion-led experiences begin to dominate how we work and live, supply chain managers will have to find different ways to respond.

With change being the only constant, those enabling the building and continuity of supply chains are playing a vital role in reshaping industry and to best position themselves for what is coming down the tracks. Harnessing the technology at their disposal to predict and prevent the obstacles that may materialise will help them to drive success.

There’s little denying we’ve entered the age of crypto. Last year, practically every crypto wallet saw its user figures increase, with Blockchain.com wallets – the site that makes it possible to buy bitcoin – boasting more than 81 million wallet users as of February 2022. And considering the array of multi-million-dollar adverts for crypto apps/currencies shown at this year’s Superbowl, it’s fair to say that cryptocurrency has well and truly entered the mainstream.

Amir Nooriala, CCO, Callsign

by Amir Nooriala, Chief Commercial Officer, Callsign

And with more people interested in digital assets, many financial institutions are rushing to create their own decentralized platforms (DeFi) to cash in on the hype.

However, this growing popularity is also fueling another boom – a boom in fraud. In 2021 alone, crypto scammers stole a record $14 billion, a staggering rise of almost 80% over 2020. And while scamming was the most popular form of crypto-related crime, theft via hacking was a close second – and not just from individuals.

The lucrative nature of digital assets has made them one of the most desirable targets for modern criminals. Yet, despite the enormous sums of money at stake, without fundamental changes to how these crypto exchanges operate – and more specifically, authenticate users – this situation is only going to get worse.

Understanding the crypto ‘Wild West’

The nature of cryptocurrency has always been antithetical to how most financial services institutions work. Blockchain technology is a dynamic, decentralized innovation, so developing the controls and frameworks to better manage it has always been a daunting task for financial services businesses, governments, and regulators (which is why many banks are still resistant to it).

And despite the public’s growing interest in crypto, many still struggle to understand the basics of how a blockchain works – they simply know it may make them rich. That confluence of poor understanding and high desirability is also why crimes – such as the One Coin cryptocurrency scam – can happen.

Detailed in the book (and podcast) The Missing Cryptoqueen, millions of people paid billion dollars for a cryptocurrency called One Coin – even though it was never really a cryptocurrency or even on a blockchain.

The leader of the company/scam, Dr Ruja Ignatova, used the confidence and excitement in cryptocurrency – along with the general lack of true understanding as to how the technology works – to prey on people all around the world looking for their own crypto success story.

However, when it comes to crypto crime, there are much simpler ways of pilfering incredible wealth without the hassle of leading a fake financial revolution. That’s because there are mechanisms enabling most of these crimes to happen, and the fault very much lies with most exchanges themselves – not individuals.

Fighting modern threats with archaic weapons

Despite the futuristic nature of crypto, criminals haven’t had to reinvent the wheel to gain access to wallets and exchanges. Because many methods of attack being leveraged by most criminals are scams that traditional financial institutions have long been aware of, such as Remote Access Trojans (RATs) and Account Takeover Fraud (ATO).

However, the problem is that crypto exchanges haven’t learnt from these techniques that fraudsters have been deploying for many years. Instead, they are deploying controls banks stopped using 10 years ago. While these controls would be fine to protect social media accounts, they are no longer enough to protect your cryptocurrencies which are now incredibly valuable.

In addition, crypto exchanges aren’t bound by the same stringent rules and regulations other financial institutions – such as banks – are. For instance, in comparison to the billions mentioned above that have been scammed from exchanges in recent months, the £1.3 billion lost by banking customers to fraudsters in 2020 is but a drop in the bucket. And that’s despite the uptick in fraud due to Covid-19.

One way crypto exchanges are particularly letting their users down is in how they conduct authentication. When these businesses want to authenticate a user’s ID, the tendency is still to use passwords and usernames, reinforced by “possession factors” – such as an OTP (one-time-password) sent via SMS message to users’ phone.

On the surface, OTPs seem like a reasonably secure method of authentication, but SIM cards were never designed for security which is why many banks have moved away from authenticating customers with them. So, credit stuffing, SIM swapping and SS7 attacks, passwords, usernames and OTPs all present fraudsters with very convenient workarounds for all the subsequent layers of security these platforms have.

But even though these are old vulnerabilities being exploited, that doesn’t mean cybercriminals are resting on their laurels – scams are getting larger and more devastating every year.

RATs for instance – whereby scammers use malware to remotely control infected computers and send/receive data from the system – are increasingly being substituted with its mobile equivalent, MRATS, to gain access to devices.

Used in tandem with other forms of attack such as credit stuffing, has proven to be incredibly effective for criminals. For instance, an ATO attack is when fraudsters use stolen credentials to try and gain access to genuine accounts, often leveraging automated tools to “credit stuff” at an astounding rate. One fraud prevention platform estimated that incidences of ATO grew a staggering 307% over just the last two years.

Simply put, it’s time for this new wave of financial institutions to stop the fraudulent activity taking place in the crypto sector under their watch. And the only way to achieve that is to uproot the broken foundation of authentication that’s currently letting its users down, in lieu of a modern solution better fitted to our digital world.

The age of biometrics

Despite the many makeovers usernames and passwords may have undergone, they’re still analogue solutions that are merely being used in a digitized context. As such, the entire notion of digital identity is built on a fundamentally broken system not built for a truly digital world.

Biometrics, on the other hand, presents a truly digital solution capable of keeping up with our dynamic world. Unlike a username or password which can be intercepted or compromised, behavioural biometrics, such as Callsign’s platform can be finetuned to individuals. It can consider everything from how a device is being held, the speed and style of keystrokes, and numerous other idiosyncrasies that are impossible to mimic.

Behavioural biometrics give businesses a method of authentication that requires no additional hardware on the part of the user (device agnostic) and doesn’t impact the user experience in any way. All while learning and adapting over time as that user’s relationship with the business evolves.

So, as crypto fraud shows no sign of slowing down, it’s now incumbent on these exchanges to interrogate the ways they authenticate users and ask themselves if their security policies are in fact putting their customers at risk. Because the sooner they can start fixing digital identities in a meaningful way, the better.