1. Immediately reassess sector macros & micros and identify sectors that have become short-term unattractive (e.g. auto), those that are now positive (e.g. pharma), and map your clients and portfolio to the new reality.

2. Segment clients as per new sector matrix, and identify clients already troubled in risk sectors and those likely to be affected.

3. Allocate above group to an expanded & high quality work-out team to co-manage the clients with existing RM’s and provide short term business guidance. Don’t necessarily do a drawn-down. In fact provide additional short term capital if needed. Refocus corporate RM teams to account monitoring, rather than new account acquisition for next 30-60 days. I would not release corporate RM headcount at this time.

4. Do all of the above for SME/Commercial accounts at a higher level of aggression. Understand the supply chain impact on your SME/Commercial clients. Get transaction banking going for SME and also corporate clients.

5. Significantly strengthen your risk, especially credit risk teams, and immediately redo the credit scorecards and algorithms.

6. Protect your liability book. Strengthen size of the corporate liabilities unit. Relook at your retail liability products and make them more attractive. Pull wealth customers in as quickly as possible.

7. On the retail side, assume 15%-30% reduction of liability and asset book, and transform operating, business and resulting cost model.

8. Digital, Digital, Digital. Strengthen your banking technology & FinTech platform & offering, and use this opportunity to aggressively move many of your customers and their transactions to digital and acquire new ones. This black swan moment is now a once in a lifetime opportunity in this area.

9. Assume 20% of the branches will need to be temporarily shut-down. Redirect customer to the other open branches. Save on branch operating cost.

10. Based on the above, make careful cost calculations by business unit from a people, process and technology perspective. Get ready to drop 15%-20% of the headcount with generous exit packages. Also compensation alignment for the remaining may be necessary.

Good Luck. And let us know if we can help in anyway.

Regards

Chairman, IBS Intelligence

Subscribe to the IBSi FinTech Journal to know more about the corona economic & banking crisis. Is it a challenge or opportunity for banking tech? Subscribe today

With digitization dotting the length and breadth of daily life, a huge amount of data gets whipped up by the hour. Every credit card transaction, every message sent, every web page opened – it adds up to 2.5 quintillion bytes of data produced daily across the globe.

This is as big an opportunity as it is an overwhelming statistic – an opportunity for even temperately clever businesses to lap up and capitalize on. Of all, Banking industry is sitting on a large piece of the pie since it generates a colossal volume of data inhouse.

The long and short of Banking digitization

It would not be a stretch to say that banking has picked up the gauntlet of digital revolution and responded with mobile and internet banking. It literally is ‘banking on the go’ with smart interfaces offering a host of banking conveniences. Some of these banks have gone a step further towards digitizing their mid and back office operations to build efficiencies and deliver seamless customer experiences. This spawn a set of scenarios:

In their bid to go digital, front-end as well back-end, banks are throwing off data by the terabytes.

This data, available on tap without any auxiliary effort remains largely unused and underutilized.

Analytics – mining this data for authentic business insights leading to better decision making is still not a priority for a lot of banks.

Digitisation to grow numbers and cut costs without insighting is taking banks only so far. To run along further, they need something more.

Data, the Differentiator

While from 1980s to early 2000s, it was IT systems that transformed the ways bank operated, today, data wields transformative potential. While it still presents itself as an untapped opportunity, it can be a critical differentiator, the one that will set the forerunners apart from the pack.

Data and Analytics holds potential in the following key areas:

Enhancing productivity – Detailed analytics can help identify lag in processes and improve efficiencies therein. It can help teams take analytics-backed decisions and respond to problem situations faster and more accurately.

Better risk assessment and management – Data analytics can help identify potential risks associated with money lending processes in banks. Based on market trends emerging from analytics, banks can variate interest rates for different individuals across various regions. Fraud detection algorithms can help identify customers with poor credit scores and erratic spending patterns to help banks take more informed decisions regarding extending loans. It may also help track dubious transactions that may be fuelling anti-social activities.

Help meet compliance and reporting requirements – Data presented in a certain way can help meet compliance, audit and regulatory reporting needs and address issues arising therein. With a super dynamic and ever-changing regulatory climate, banks and financial institutions need a robust backing to be able to meet all requirements on time and with precision, and data and analytics can play a decisive role in this.

Delivering an omnichannel banking experience – With customers interacting with banks through multiple channels, a seamless and consistent experience at all points in the chain is crucial and data analytics can help drive this with efficacy.

Detailed nuanced understanding of customers – Analytics can enable a detailed profiling of customers based on inputs received from their spending trends, investment patterns, motivation to invest and personal or financial backgrounds. This opens opportunities to personalize banking solutions, integrate customer acquisition and retention strategies and cross-sell & upsell. It can also be a crucial input for risk assessment, loan screening, mortgage evaluation etc.

Realising the Data Dream

Data and Analytics can prove to be quite the enabler for banks that are ready to reinvent themselves. But the data dream can be as elusive as it is promising. A piecemeal approach that moves from one project to the next under can yield results below encouraging. It is important that the business leaders envision what problems they want to solve with data and analytics and get involved every step of the way. A great analytics approach starts at asking the right questions to guide the discovery process, before data is dived into for the sake of it.

By Kiran Kumar, Co-Founder and Executive Director of Profinch Solutions

Governments globally have woken up to the seriousness of the problem that COVID19 (Coronavirus) poses and have put in place adequate emergency responses. On our part, we should follow the best practices and ensure to contain the spread. The first lesson for all of us is not to be tone-deaf. While crashing markets in bad times are an excellent opportunity to buy, as a community, we must collectively wish and actively work towards making things better. So, stay healthy, sit tight, and spread awareness where you can. The second is to only rely on authentic sources like WHO or CDC. It is not the time to forward everything you receive on social media without verifying authenticity. “Forwarded as received” does not absolve you from your duty as a concerned global citizen.

Investments during the time of global crisis

These are extraordinary times, and while markets have retraced 20% or more many times before, the speed with which this retracement has happened is a first. It took S&P 500 a mere 16 sessions to drawdown 20% and entered the bear market territory. Global markets are spooked, and so are the Indian equity market. The co-incidence of YES Bank fiasco, in India, playing out at the same time doesn’t make things more comfortable as it impacts investor confidence. However, as we have seen many times before, human and economic resilience is immense, and sooner or later markets do bounce back to reflect the constant march of progress.

Surprisingly for an individual investor, what works in peacetime also works in times of distress such as COVID19. I started working and investing during the dot-com bubble and was trading CDS during the great financial crisis.

Do’s & Dont’s for retail investors

Below are five lessons I have learned to keep one’s personal investing simple. Simplicity matters, because just as in dieting, it is better to follow a diet you can follow for decades than one that requires extraordinary effort for immediate but fleeting benefits.

Stick to your asset allocation and rebalance if it gets off by 5%. We will send reminders when that happens. In a crash, you will sell your debt and add equity. It may appear counter-intuitive, but it is not. You are buying more equity as it falls.

Track your wealth and not just your portfolio. At a wealth level, last month’s ~20% decline in Equity Mutual Funds is still only a 5% decline in average wealth as gold has rallied.

Postpone all decisions by two days. Say you are itching to buy or sell or stop a SIP or increase your SIP. Write the resolution down and revisit it in two days. You will make better decisions.

Check your wealth once a week. Yes, that’s right. The more you check, the more you will think you need to do something. Inaction is not our strength.

If you have itchy hands, buy Rs 100 in any index fund. Always buy, always make it a trivial amount. It satisfies your urge to take action without making any difference to your long-term outcomes.

Stay away from false narratives

While putting a timeline on the severity of the drawdown or that of the recovery is near impossible, following these best practices will help protect your wealth and survive such market crashes. In hindsight, this week will be another example of not making investment decisions in the heat of the moment. If you got whipsawed by the price movement, then consider it a learning lesson. As an investor, don’t punt on daily price moves. Don’t fall into the false narratives of fading a big move or catching a rally early – especially if it is coming from an expert. The winning strategy is to keep it simple and stay invested.

(Disclaimer: The views and opinions expressed in this article on Coronavirus (COVID19) are those of the author and do not necessarily reflect the views of IBS Intelligence. Kuvera.in is a wealth-management company regulated by the Indian financial regulator SEBI)

1. Financial Services sector stability & profitability comes under pressure – stock valuations and prices come down.

2. Central banks bring down interest rates – if a significant part of the asset book is flexible rate, then interest margins are affected.

3. Lower business and consumer transactions – lower fee income.

4. Less liquidity from government as they need to finance deficits. And deferred spending – negative liquidity impact.

5. Number of corporate banking sectors negatively affected. Example – oil & gas, consumer durable, automotive. Increased number of work out accounts, likelihood of NPAs, and reduced income.

6. SME/Commercial clients under pressure for many sectors – reduced demand and delayed payments from customers. Larger number of NPAs, work out accounts, and reduced income and a smaller trade finance book.

7. Wealth Management not so wealthy any more. Portfolio values down. AUM down. Conversion to cash preserve capital. Resulting in fee income reduction. Also margin calls.

8. Retail book stressed. Less liquidity, and asset quality under threat. Part of mortgage book impacted. Reduced spends on cards, auto and personal loans. Loss of income also resulting in higher NPAs. Also limited growth.

9. Branch utilization drops off – fear of visit, fewer transactions.

10. Basically the full revenue & cost model affected – urgent need to transform, including job losses.

Potential winner – digital channels and digital banking ? Read the fixes and the suggestions for the best way forward out of this crisis in the next memo !

Regards

Chairman, IBS Intelligence

Subscribe to the IBSi FinTech Journal to know more about the corona economic & banking crisis. Is it a challenge or opportunity for banking tech? Subscribe today

When the world’s second-largest economy gets hit, the tremors are bound to be felt by both large economies such as the US and developing ones like our own.

The Coronavirus (COVID-19)epidemic, with its epicenter in Wuhan, the capital of the busy province of Hubei in China, has claimed more than 3,000 lives and infected over 90,000. It has spread to over 60 countries and sent shockwaves through financial markets. Beyond its pathological implications, lies its impact on the global economy.

The Indian angle

The trade between China and India is worth $87 billion, of which we import goods worth $70 billion from China. It includes everything from electric components and machines, medical instruments and pharma raw materials, vehicles and auto parts, iron and steel components to nuclear machinery.

While China takes 5.1 percent of our total exports, in the form of cotton, salt and organic chemicals, and mineral and metal ores among others, we get 13.7 percent of our total imports from China alone.

Needless to say then, when our second-largest trading partner hits the brakes on its factory output, companies in India break into a sweat.

We may have pushed for smartphone manufacturers to increase their domestic production, but they still depend on China for their components. Other electronic goods manufacturers would also be facing production issues.

A supply shortfall in consumer electrical and electronic goods in India (either due to coronavirus-led Chinese cuts or our economic slowdown) would also trouble online sales, as they form a sizable portion of e-commerce goods sales.

Pharma companies bring in key raw ingredients from China to make medicines. Automobile manufacturers, too, are heavily dependent on their components on their Chinese suppliers.

However, the Chinese New Year in January-February would have proved to be a greater boon than usual as companies would have stocked up by December last year, anticipating the Chinese holiday season.

Goods and services

Goods and services across the world are suffering the aftermath of the quick spread of the Coronavirus (COVID-19). Global exports and imports and Chinese exports and imports are so intertwined that it is unavoidable.

The spillover of disruption has been the most acute in China’s neighbors as seen in their monetary policy responses.

Impact of Corona Virus, DBS Report/Tavaga

Goods movement

Shipping has been heavily affected with curbs on movement to stem the spread of the Covid-19 virus.

Shipping companies have cut back on their ships sailing from China to the rest of the world, carrying goods, to prevent the virus from advancing to other areas.

It has a direct bearing on the world’s supply chain as 80 percent of global goods trade by volume is transported in ships and China itself houses seven of the world’s 10 busiest container sea-ports, says the United Nations Conference on Trade and Development. The contagious coronavirus is a threat to business infrastructure in adjoining countries as well, as Singapore and South Korea, too, have busy ports and have seen the disease escalate.

Global GDP

The global GDP will be compromised due to the economic fallout of the coronavirus. China accounts for around 18 percent of the global GDP (2019) compared to 4 percent when the Sars epidemic had broken out in 2003. Chinese businesses are now more ingrained in global supply chains.

Sars had robbed China of 1 percent of its economic growth in the eight months it had lasted. The coronavirus is expected to shave off 1-2 percentage points off China’s GDP growth in the first quarter of 2020.

Investor takeaway in times of epidemics

Contagious epidemics such as Coronavirus (COVID-19) bring uncertainty to the investing community worldwide, prompting them to move towards traditional assets such as golds and bonds that are perceived to be more stable, instead of the assets with systemic risk like equities.

That is where smart investment planning involving diversification and asset allocation comes in. It allows us to stay out of troubled waters and focus on our health, instead.

(Disclaimer: The views and opinions expressed in this article on Coronavirus are those of the author and do not necessarily reflect the views of IBS Intelligence.)

Machine learning and associated algorithms are making real waves not just in banks’ front offices but also in analysing and spotting trading opportunities in the stock markets.

Machine learning (ML) is being used to identify trading patterns, initially in historical trade and quote data. This may sound familiar to those who are cognisant of technical analysis and the end goal is indeed the same, that is, to find useful patterns in historical and even real time data that lead to decisions that may result in profitable trades either long or short.

According to Tom Finke, head of machine learning product management at software and data provider OneMarketData: “What’s different now is that the techniques have evolved in performing that analysis. In particular, we are able now to use machine learning algorithms to help improve some of the more historical sorts of algorithms that were used to try to detect patterns. When we train machine learning models, such as neural network models, they are able to find patterns that traditional analyses like regression analyses might not otherwise find. These sorts of algorithms are able to find patterns that mere humans are not able to find because of the extent of the vastness of the data that can be analysed.”

An arms race?

Of course, if every trader was to follow the same analytical signals they would all be doing the same thing at the same time. Finke admits that funds, brokers, trading firms, banks and asset managers are facing a “sort of arms race”! He added: If you don’t participate, there is a risk, you’ll indeed be left behind. It would be advisable for investment firms and investment funds that want to stay on top of things that they really should form teams to at least investigate how machine learning can help with their investment and trading decisions.”

But the machines are not completely taking over, well not yet. “It takes some human ingenuity and cleverness, to decide the parameters around those machine learning algorithms. For example, what is the most appropriate data set on which to build a machine learning model?”

Right now, the human element is still required. It takes a person to decide which ML algorithm should be used and what pool of data should be analysed. However, there are companies working on this with ML algorithms being developed with the aim of having them choose which are the best ML algorithms to use.

Watching the markets move

With algorithms being used to analyse trading patterns it should come as no surprise that one way this is being leveraged is in market surveillance. OneMarketData’s core product is a time series tick level database on which that company had built various vertical applications – one of the most popular being trade surveillance.

“We have that particular application being used by a major exchange in the US and by quite a few investment banks. They’re analysing order books; some historically and a few in real time to try to detect patterns that are nefarious such as spoofing or layering [both forms of illicit manipulation in which a trader may attempt to deceive others regarding the true level of supply/demand for a given financial instrument]. Traditionally there are patterns that you can look for and detect to try to find these activities and now we are in the early stages of applying machine learning algorithms to that,” said Finke.

One thing that has changed in the financial markets in the last few decades is the sheer volume of data and number of trades. Finke noted that in the last week of February 2020 when the world’s financial markets became seriously ‘spooked’ by concerns over the global Coronavirus (COVID-19) outbreak, the number of ticks during the volatility was such that “some of our customers were running out of memory in their memory databases”.

Seeking the right signal

ML and the appropriate algorithms are capable of analysing more than just price data. For example, Bloomberg now provide a machine-readable news feed that is tagged to make it easier for computer software to parse the text.

This parsed news may then be stored in the same way as trader quote ticks. Run it through a natural language processing algorithm to parse it into meaningful chunks (a technical term!) and then as stage two use another ML algorithm to decide whether there is enough information to provide a trading signal… and if there is, what should that signal be?

Such algorithms are being developed with the analysis of historical data but once the models are trained, they can be applied to real time streaming news data to try to generate real time trading signals. Sure-fire success in such endeavours is by no means guaranteed. “This still a hard problem. It’s hard for humans, it’s hard for anybody to pull meaningful market sentiment out of newsfeeds. We’re still in the early stages of having any sort of effective results, but that’s certainly not stopping people from making the attempt,” concluded Finke.

#1 INNOVATE The world is changing faster than you think. Being distinctive and innovative is key to your survival and success. Create a top 10 list of innovation ideas you can implement across all functions of your business in 2020 and get it done. As Nike says, Just Do It!

#2 FOCUS, FOCUS, FOCUS Focus is everything is life. Nothing can be achieved without focus. Pick the areas you want to go after and then put all your resources behind them. The real challenge will be – can you stay disciplined and avoid the distractions? Sometimes it is better to have the blinkers on!

#3 DRIVE ENTERPRISE VALUE Customer is king, and your human capital is valuable, but what about the shareholder? Time to give them some tender loving care. Listed or unlisted – track your enterprise value monthly. More importantly, for every main strategic initiative, ask the question – how will it drive enterprise value?

#4 IT’S ALL ABOUT THE CASH Cash still remains king. Sometimes it good to learn some lessons from the often criticized PE industry. Measure your business on cashflow. Run it like a shop. When your shutter goes down at night – how much cash did you bring in?

#5 DISCARD & ADD Too many companies sink under the weight of too many products they like to sell. 20% of products generate 80% of revenue. The tail is always too long. Have the guts to discard products that don’t generate revenue and add selectively to drive your innovation agenda.

#6 ONLINE IS KING Your channels are changing as you sleep. While your office and stores are shut, the customers are at play. Fastest finger first on their favorite online sites. Make being a best-seller on the #1 online channel your priority. Getting online right could make the difference on whether you live or die.

#7 THE NEED FOR SPEED Patience is out of style. Customers want everything now. Clients wanted it yesterday. If you can’t take care of them, somebody else will. Online has made the world flat. Crash the turn-around-times of every key process in your organization. Go Formula 1!

#8 UNLOCK YOUR HUMAN CAPITAL People are important, but not at the price of success. Structure right, have the right headcount and competency, but more importantly create a performance oriented organization. Reward the performers and clean up the tail every year in a humane way – yes, it is possible to do both together.

#9 GO COOLTECH, GO DIGITAL The world has gone digital. Maybe this time the trees can really be saved. Automate to the maximum. Word’s like AI, Machine Learning, Robotic Process Automation are not Latin anymore. Simple applications using these technologies are available for all businesses. Use them. The robots have arrived!

#10 WORK & LIFE CAN BE BALANCED! It’s true. Starts with your cell phone. Look at it every hour or two during the work day and once every evening at the most. Twice on the weekend. Sorry I can’t be more generous. And focus your free time on your family and friends – not Netflix. It is possible to work hard and play hard.

Have a great 2020, and see you on the other side of the calendar!

2020 is almost here, and it is a perfect time to look back on 2019 and appreciate the highs and lows. By this point in 2019, the words ‘FinTech’, ‘Data Science’ and ‘Machine Learning’ have become relatively common, and implications attached to these words have become apparent to anyone who is a part of the modern world.

FinTech in India has been growing at a significant pace for the last four years as a result of the increasing focus from RBI, government policies, advancing technology and affordable smartphones and data.

In turn, the Indian FinTech ecosystem has finally matured with the public at large, becoming more receptive towards digitization and tax automation. This is owing mainly to the demonetization of 2016 and the introduction of the Goods and Services Tax in 2017. In fact, implementation of GST alone has led to dedicated startups and new business verticals from established brands to help small, medium and large businesses with their taxes.

2019 was expected to be a year with continued momentum, but it came with its share of surprises. The industry did not grow as fast as anticipated, but like everything else in life, there were also moments of delight.

Firstly, the IL&FS liquidity crisis led to a massive trickle-down effect on NBFC lending, which led to a considerable reduction in available debt to smaller NBFCs. Liquidity is the raw material for financial services, and in the absence of a steady supply, many FinTechs grew slower than expected.

Secondly, RBI continues to be silent on some key issues like e-KYC, e-sign, e-NACH, which were the catalysts for a seamless journey and growth. The circulars were expected to post the elections, but that has been delayed, leading to a lack of clarity.

Thirdly, UPI and Payments saw a great deal of growth and investments coming in. UPI has been recognized globally as a masterpiece of innovation. With 143 banks live on UPI clocking 1.2Bn transactions in November alone, it has completely transformed the way money moves in India.

2019 was also a year with many FinTechs building real-time, fully automated and intelligent solutions for lending and payments. AI and Machine Learning saw some real takers and many human-led processes were fully automated.

As liquidity continues to come back and wait for RBI continues to streamline KYC, the trends I see shaping fin-tech startups in 2020 involve a highly aware customer and further innovations in data science and data engineering.

Trend 1: India is rapidly moving towards a mobile-first approach for accessing financial services, and they prefer vernacular platforms.

With a 400Mn reach of WhatsApp and thousands of hours of content being created by OTT platforms – Indian consumers are online on their smartphones. YouTube in India has over 1,200 channels with one million subscribers, and this number was only 14 in 2014.

This provides an unparalleled opportunity for tech companies to build digital journeys and solutions to disrupt almost everything that we know today. Financial Services, Transportation, Logistics, Shopping, Telecom, Healthcare, Education are all going to see newer players challenging the status quo. There is nothing called Digital Strategy now, it’s just Strategy to survive in a Digital India!

FinTech also is witnessing the same behavioral shift where 95%+ users apply for a loan using a mobile device while this number was less than 30% three years ago. We have seen a 2X conversion on our vernacular pages compared to English landing pages.

Trend 2: Data Science and Engineering are delivering substantial cost efficiencies and better decisions with cutting edge applications of Computer Vision, Optical Character Recognition and Pattern recognition.

FinTech is growing at an exponential pace in India with high applications of data science in aspects like lending, insurance, broking and wealth management. Several lending companies have used image, text, and voice as input data sources to provide accurate decisions and better experiences than their banking counterparts in the last couple of years in India. Optical Character Recognition was meant to read the text inside images and transform that into digital text data. Now, there is an integration of OCR in our daily lives – from scanning documents and credit cards to data entry. The traditional, time-consuming paper-based work has been replaced with an optimized way of collecting the same data. With the enhanced ease in collecting data, data scientists can start their analysis journey quicker.

Data Science and Data Engineering are working more closely than ever with T-shaped data scientists becoming popular by the day.

Being one of the youngest nations in the world, a considerably large section of the Indian population is significantly more receptive and adaptive. The result is tech-savvy zealous entrepreneurs pushing the Indian fin-tech industry towards potential earnings to the tune of US$ 2.4 billion by end 2020.

Billed as a game changer by most in the industry, Open Banking witnessed a managed roll out in the UK in April 2018, paving the way for customers to experience enhanced banking services through a variety of authorised providers. The Competition and Markets Authority ushered in Open Banking with the aim to improve the quality of banking and financial services, ensuring banks remain customer-oriented in an extremely competitive market.

Optimistic market forecasts estimate that Open Banking could generate more than £7.2bn by 2022 if various sectors tap into its massive potential.

Open Banking allows secure data sharing by using an integration technology called Application Programming Interface (‘API’) that accesses the account and transaction information of customers and even allows third party providers (‘TPPs’) to initiate payment on behalf of customers, only upon their explicit approval.

As we move into 2019, what has actually changed and what lessons can we learn? Has this ‘great disruptor’ in the banking sector lived up to its initial hype?

A Closed Mind to Open Banking

The CMA reported that in June, there were 1.2 million uses of Open Banking APIs, describing it as a slow but positive start to changing consumer attitudes and revitalising the banking ecosystem for the better.

However, one senior source at a financial technology company told The Daily Telegraph: “The lack of promotion by the big banks has been disappointing and it’s the main reason for the slow take-up”.

So what are the reasons for the slow start? Why are the big banks taking their time?

Anne Boden, CEO and founder of Starling Bank, has been quoted as saying that the big banks “are all using legacy technology that’s 20, 30 or 40 years old… there’s no commercial reason why they want to do it [Open Banking]. Without that it’s a very difficult thing to do.”

Though public sentiment towards Open Banking is far from effusive, do remember it is a complex change that will take time to transform the way banking is done. Open Banking inherently brings a raft of technological and economic risks for the traditional banking model and navigating those changes is going to be an uphill task. One of the biggest teething problems faced in the banking sector is the legacy technology that is still used in the major banks, preventing them from quickly benefiting from this ambitious regulatory-driven process. In some instances, the technology could be even thirty or forty years old. The cost of overhauling their legacy technology to allow integration with API is prohibitively high, adding further traction to the process of adoption. However, if banks and financial organisations are eager to monetise the myriad opportunities presented by Open Banking, they need to be quick about overhauling their systems and IT infrastructure. Further, they also need to constantly innovate and bring out banking apps and other technology-driven solutions to enhance the banking experience for their customers.

Though the CMA provides guidelines on security measures and details of regulated providers, it still fails to address the underlying issues of legacy technology to ensure that there is no loss in the transfer of customer data.

Driving the Change

Banks own valuable customer data and are fiercely protective of it. Also, consumers who are not familiar with the actual applications of Open Banking are reluctant to embrace it as they fear fraudulent transactions and other complications arising from this technology. Adding to this hurdle is also the lack of awareness of the risks and benefits associated with Open Banking that has limited its appeal among the masses.

Therefore, the challenge for the banking sector is in implementing these concepts on the ground. Any compromise on customer data will not only result in regulatory penalties but also in the damaging press. No wonder then that cyber and data security rank amongst the top priorities of every Bank CIO and CEO.

Since Open Banking requires banks to share detailed customer information (other than sensitive payment data), they are required to undertake due diligence while sharing the same, even under the express consent of the customer. Banks and TPPs need to ensure customer consent is taken with due emphasis on the customer’s ability to understand and appreciate the possible outcome from the provision of their data. Since banks are deemed to be the final custodian of customer information, they have to secure their systems against financial crime, fraud detection and AML, among other things. Further, a bank’s IT infrastructure will need to be more secure and resilient as it will now be exposed to threats ported through TPP systems. They have to invest more effort and energy to analyse and discover potential points of vulnerability and take adequate measures to address this holistically. Core banking systems need to adopt open API based peripheral development, delivering quicker implementation cycles and minimal customisation of the core product. Furthermore, the industry’s adoption of API standards should set a benchmark for all involved parties. Banks and TPPs should adhere to and promote development in line with these standards.

Finally, it is worth mentioning that many large payment systems and core banking providers have developed Open Banking-compliant solutions. Without going into a lengthy debate on the merits and demerits of each of them, it might suffice to recognise that these systems, along with robust identity and access management systems, can comprise a strong first line of defence for the Open Banking ecosystem.

The Best Has Yet to Come

While the consumer experience may not have altered significantly in the initial rollout of Open Banking, experts opine that it won’t be long before the positive effects of this innovative model trickle down to the end users.

Already, the market is charged with competition and has become riper for innovation. Positive changes are taking place internally and banks are strategising to become more customer-centric and proactive. This will bode well for the long-term relationships banks have with their customers. As we gear up for the next wave of Open Banking, we hope that its innovative model will lead to a level playing field for both customers and banks. For once, innovation will go hand in hand with pragmatism and plain grit, to script the winning equation for the future of banking.

By Shuvo G. Roy, Vice President & Head – Banking Solutions (EMEA), Mphasis

The digital banking space has always been a hotbed of tech innovation, with almost every new tool putting customer comfort and convenience at its core. And why not? After all, the customer is king.

Wait. Scratch that.

The New Age business idiom has changed – now, the customer is a comrade. Smart financial institutions are building a sense of camaraderie with customers to enhance banking experience. For this, they’re turning to Artificial intelligence (AI).

Enter the chatbot.

The most effective chatbots – essentially computer programmes designed to simulate human conversation – are designed to make life breezy for the busy customer. To be like that finance-savvy friend – only, all smarts and zero sarcasm. Programmed to take requests, offer insightful advice and even crack the occasional bad joke (check out the philosophically quirky chatbot created by National Geographic to promote Genius, their show on Albert Einstein), chatbots are all about Empowering through Experience.

For a bank customer, this could mean:

Personalised assistance: Chatbots can simplify banking for customers by opening a new account, making money transfers, paying bills online – without going through multiple steps and checks. They can be intuitively programmed to provide personalised alerts based on customer habits and preferences. Salary credited. How about investing in a Fixed Deposit? Credit card outstanding settled. How about finally placing an order for that Bose sound system you’d been Google-ing for the last one year?

Round-the-clock support: I have a friend who often has nightmares that every cheque she’s written has bounced because she’s exhausted her salary account mid-month. What she needs is a chatbot to allay her fears, instantly, even if it is after business hours. So, imagine her having this rather reassuring text exchange with a banking chatbot at 2am:

Chatbot: Hello, Priya. How can I help you today?

Priya: How I am doing with my salary account till my next payday?

Chatbot: Well, you have a phone bill of Rs 2,238 due tomorrow. The balance thereafter would be Rs 43,034.

Priya: OK. And could you please transfer Rs 10,000 to my Demo Bank savings account right now?

Chatbot: Done. Your Demo Bank savings account balance is Rs 53,000. Do you want to add Rs 7,000 more and round it up to Rs 60,000?

Priya: Sure.

Chatbot: Done. The balance in your Demo Bank savings account now is Rs 60,000. That’s Rs 12,000 more than it was this time last year. Good going!

Financial guidance: Money management is a challenging landscape for a lot of people. Especially millennials with a multitude of options to choose from. For this lot, chatbots can help make choices based on their needs and financial health. Erica, the Bank of America chatbot, for instance, shares tips on how customers can save better by cutting certain expenses and even offers advice on how much they can afford to spend based on their current financial status.

While they definitely give customers more bang for their buck, chatbots can also have financial services providers laughing all the way to the (…well) bank. Creating well-strategized chatbots could mean:

Customer loyalty: Bringing in a personal touch, through services like 24-hour assistance and financial advice, can win over customers.

Customised marketing strategy: Information collected by chatbots during interactions with customers can be leveraged to deliver personalized suggestions and push targeted products based on customer profile and preferences.

Brand building: Chatbots can be designed to personify the ethos of an organisation – no-nonsense and business-like or casual and cool – and build brand identity.

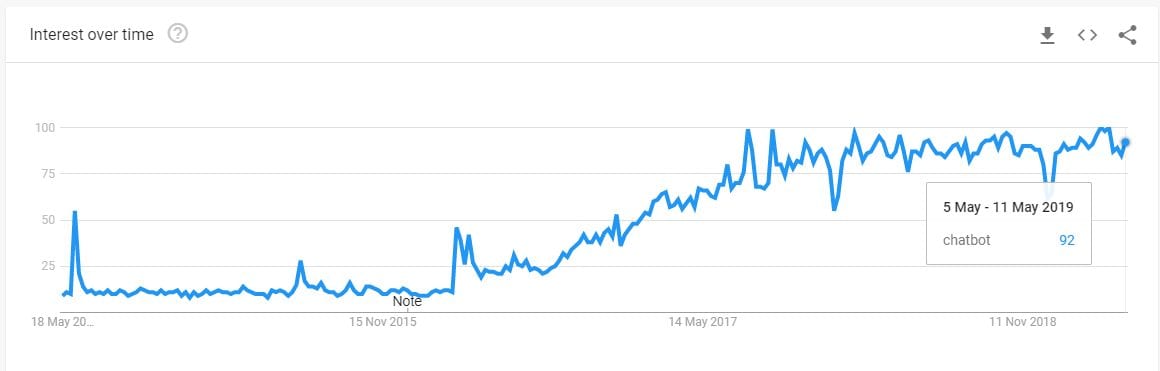

The conversation around the use of artificial intelligence in business and service delivery is not new. However, what is heartening is that the interest hasn’t waned. Google Trends data shows that the chatbots narrative is still buzzing. If you are not part of this story yet, get on board ASAP – because the best is yet to come.

By Padmanabhan R, Head of Product Management, Clayfin